How to Set Up A Trust For An Elderly Parent: 6 Easy Steps

Joel Lim

June 6, 2023

|

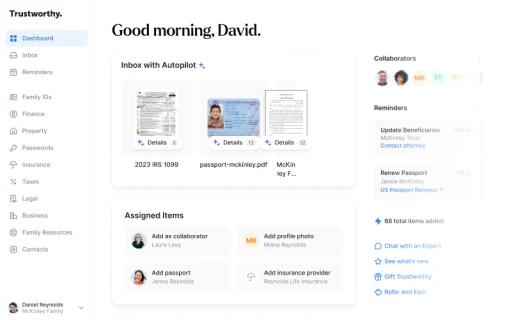

The intelligent digital vault for families

Trustworthy protects and optimizes important family information so you can save time, money, and enjoy peace of mind

By setting up a trust for your elderly parent, you can ensure proper, reliable management and handling of your parent’s assets.

So, now you might be wondering how to set up a trust for an elderly parent. That’s exactly what you’ll learn. This article details trusts, their process, and the best way to set one up.

Key Takeaways

Setting up a trust has several benefits, including reduced taxes on procured assets, no probate costs, and protection from scams.

There are several types of trusts to consider, such as revocable, irrevocable, living, testamentary, and special needs trusts. In most cases, an irrevocable trust is the best choice.

Although you can, we would not recommend setting up a trust on your own. Hiring professional guidance to help you with your trust ensures legal compliance and correctness and will save you from any complications in the future.

What is a Trust, and Why Set One Up for an Elderly Parent?

A trust is an arrangement to organize and distribute the assets of a living “grantor.”

A trust involves three parties:

The sole grantor is the legal owner of the assets listed in the trust. In your case, your elderly parent will be the “sole grantor.”

The assets are divided and set to be distributed to the beneficiaries. The beneficiaries can be you, your siblings, family friends, or anybody with a relationship with your parent.

The final role is the trustee. The trustee is responsible for allocating and distributing the assets per the trust after your parent passes away.

There are several benefits to setting up a trust. These benefits include:

Protection from scams, self-management mistakes, and fraud: As your parent gets older, they are more likely to be targets of scam and fraud schemes. They also might lose their ability to manage their finances properly. A trust can protect them by giving control to a more knowledgeable and careful trustee.

Heavily reduced taxes on procured assets: Taxes on assets gained in a trust, like property tax, are much less than those given away during somebody’s lifetime.

No probate costs and no court proceedings: Through a will, the assets and finances of your parent will be distributed through court proceedings. The costs of these proceedings are known as probate costs, which are not applicable or necessary for trusts.

Step #1: Understanding the Different Types of Trusts

Before getting started, it is essential to understand the different types of trusts.

Each type has its specific use and implications.

After you understand each type of trust, you can decide which type will benefit you, your parent, and other beneficiaries the most.

Revocable Trusts

Revocable trusts appoint the grantor as the trustee until they can no longer manage the assets.

This could be through passing away or incapacitation. The grantor designates a successor appointed as the trustee upon the passing or incapacitation.

This type of trust protects your parent by still allowing them a degree of control over their assets. They can edit and adjust the trust as they please. This protects your parent from other beneficiaries or non-trustees from changing the trust in unfavorable ways.

Irrevocable Trusts

Irrevocable trusts involve your parent, the grantor, giving up control to the trustee and other beneficiaries. Unlike revocable trusts, only beneficiaries can edit the trust, not your parent. Your parent will hold ownership of the assets listed on the trust until their transfer to the beneficiaries.

The significant benefit of an irrevocable trust is that it may not affect your parent’s ability to qualify for Medicaid.

This protects your parent from selling or relinquishing any assets to qualify. If their assets produce any income, they will not be subject to taxation for that income. It can also ensure your parent’s spouse does not lose their home upon passing away.

Testamentary Trusts

A testamentary trust protects your parent if their spouse passes away. When this happens, your parent’s assets are transferred into a testamentary trust, where they will have no control over them.

This type of trust is supposed to protect your parent from fraud and scams and allow them to live without worrying about finances.

Special Needs Trusts

A special needs trust ensures your parent remains eligible for disability benefits while still allowing them to receive income from their assets. Your parent can appoint you or a trusted third party as the trustee where you are responsible for the assets listed.

Special needs trusts are divided into two categories: first-party and third-party trusts. Your parent will be listed as a trust beneficiary. They will receive their own income from any assets, but this income will not affect their eligibility for government benefits.

A third-party trust is where the income is provided by a third party, not from your parent’s assets. The third party can be you and your assets or any other funding source your parents receive.

Step #2: Choosing a Trustee for Your Parent's Trust

Choosing a trustee is one of the most critical decisions when drafting a trust. There are a few factors you must consider before making your decision.

The first factor to consider is the expertise of the trustee.

The trustee will be responsible for all of your parent’s assets. Any errors can mean hefty fines or complications for those involved with the trust. Choosing a family member or individual trustee may cost less, but corporate trustees are safer and ensure compliance and correctness.

The next factor to consider is cost.

To hire a corporate trustee, you will likely pay 1-2% per year for their services. All of the insurance and compliance regulations are included. Compared to hiring a family member or individual trustee, it will likely cost more. However, individuals may hire outside sources, such as accountants or attorneys, to assist in their management.

The other factor is objectivity.

If you choose a family member as the trustee, their decisions may be biased or emotionally charged.

Complex relationships between family members and personal feelings can influence their decision. Corporate trustees are more objective-based but do not have insight into the family.

Related Article: What To Do When A Sibling Is Manipulating Elderly Parent

Step #3: Drafting the Trust Agreement

Drafting a trust agreement may be more straightforward than you think.

The first step is listing all assets your parent wants to include on the trust. This could be property, stocks, bank accounts, physical objects, or anything your parent “owns” and wants to pass on.

The next step is to secure the necessary paperwork associated with the assets to prove ownership. This includes deeds, certificates, titles, and other proof of ownership.

That’s where Trustworthy can help you. We secure and organize important family information, from IDs to money and property information.

After that, you must assign the roles of a trust.

Your parent, alone (not including their spouse), is the sole grantor. Next, your assigned trustee to manage the assets, and finally, the beneficiaries who will receive them.

Once you have the roles assigned and the necessary paperwork, the last step is to fill out the trust document following your state’s laws.

Step #4: Funding the Trust and Transferring Assets

The funding process will differ depending on the type of asset you wish to add to the trust.

However, most physical assets require a simple document to fund all assets in a broad category. For example, all “cash,” “furniture,” or “clothes.”

You require the specific documents outlined in the relevant organization's process to transfer assets like property, business stakes, or finance accounts.

For example, banks typically have designated forms to fill out to transfer a bank account to a trust. The property will require the deed or title of ownership to be transferred.

Contact all parties and companies involved if you have a more specific or complex situation. They will likely tell you directly what is required for them to be able to transfer the asset.

Step #5: Managing and Distributing Trust Assets After Your Parent's Death

After your parent passes away, the trustee will notify the necessary organizations and file the trust with the probate court.

The organizations that need to be notified are the social security administration and the Department of Health. Next, the trustee will notify the beneficiaries of the passing.

The trustee, if responsible, will pay off the grantor’s debts before finally distributing the assets according to the trust’s will. The trustee must legally distribute the assets exactly as the trust dictates.

It is also important to note that depending on the type and amount of the asset a beneficiary receives, they may have to pay taxes for the additional capital.

You should include additional capital, property, or assets when you file your taxes. If not given by a trustee, the beneficiary can legally request exact amounts and values of any assets they receive to aid in filing taxes correctly.

Step #6: Seeking Professional Guidance and Advice

We highly recommend professional guidance to help in the drafting process, distribution of assets, and legal matters. Professional guidance or advice will ensure legal compliance to avoid complications after receiving or distributing assets.

You can request the assistance of trust attorneys, corporate trustees, accountants, or financial advisors. Contact a professional and assemble the relevant documents before drafting your trust. The extra cost will save you effort and ensure a smooth process.

Frequently Asked Questions

What is the best trust for older people?

The best trust for older parents depends on your parent’s specific needs.

A revocable trust will allow them to edit or cancel it anytime. It also protects them from outside forces or beneficiaries from changing the trust. With a revocable trust, your parent can also assign a trusted successor trustee.

On the other hand, an irrevocable trust may not affect your parent’s ability to qualify for Medicaid. It also protects their assets from taxation and ensures the spouse does not lose their home upon passing away.

What type of bank account is best for a trust?

You can set up a trust account at your bank to deposit into or make payments from. The account will not belong to any individual but will be under the trust itself. This ensures the money in the account is subject only to the wishes of the grantor outlined explicitly in the trust.

What assets are best in trust?

The best assets to include in a trust are bank accounts, property, business equity, physical objects, insurance policies, and bonds or stocks. These assets will provide for easy distribution to beneficiaries and avoid excessive taxation.

What is the negative side of trust?

The downsides of a trust are the seemingly complex process and decisions that go into its creation. Giving up control of your assets can be scary, and a trust requires detailed and exact information to be considered legal and valid. There is also the risk of losing tax benefits or being subject to extra taxation with the transfer of assets.

How to Set Up A Trust For An Elderly Parent: 6 Easy Steps

Joel Lim

June 6, 2023

|

By setting up a trust for your elderly parent, you can ensure proper, reliable management and handling of your parent’s assets.

So, now you might be wondering how to set up a trust for an elderly parent. That’s exactly what you’ll learn. This article details trusts, their process, and the best way to set one up.

Key Takeaways

Setting up a trust has several benefits, including reduced taxes on procured assets, no probate costs, and protection from scams.

There are several types of trusts to consider, such as revocable, irrevocable, living, testamentary, and special needs trusts. In most cases, an irrevocable trust is the best choice.

Although you can, we would not recommend setting up a trust on your own. Hiring professional guidance to help you with your trust ensures legal compliance and correctness and will save you from any complications in the future.

What is a Trust, and Why Set One Up for an Elderly Parent?

A trust is an arrangement to organize and distribute the assets of a living “grantor.”

A trust involves three parties:

The sole grantor is the legal owner of the assets listed in the trust. In your case, your elderly parent will be the “sole grantor.”

The assets are divided and set to be distributed to the beneficiaries. The beneficiaries can be you, your siblings, family friends, or anybody with a relationship with your parent.

The final role is the trustee. The trustee is responsible for allocating and distributing the assets per the trust after your parent passes away.

There are several benefits to setting up a trust. These benefits include:

Protection from scams, self-management mistakes, and fraud: As your parent gets older, they are more likely to be targets of scam and fraud schemes. They also might lose their ability to manage their finances properly. A trust can protect them by giving control to a more knowledgeable and careful trustee.

Heavily reduced taxes on procured assets: Taxes on assets gained in a trust, like property tax, are much less than those given away during somebody’s lifetime.

No probate costs and no court proceedings: Through a will, the assets and finances of your parent will be distributed through court proceedings. The costs of these proceedings are known as probate costs, which are not applicable or necessary for trusts.

Step #1: Understanding the Different Types of Trusts

Before getting started, it is essential to understand the different types of trusts.

Each type has its specific use and implications.

After you understand each type of trust, you can decide which type will benefit you, your parent, and other beneficiaries the most.

Revocable Trusts

Revocable trusts appoint the grantor as the trustee until they can no longer manage the assets.

This could be through passing away or incapacitation. The grantor designates a successor appointed as the trustee upon the passing or incapacitation.

This type of trust protects your parent by still allowing them a degree of control over their assets. They can edit and adjust the trust as they please. This protects your parent from other beneficiaries or non-trustees from changing the trust in unfavorable ways.

Irrevocable Trusts

Irrevocable trusts involve your parent, the grantor, giving up control to the trustee and other beneficiaries. Unlike revocable trusts, only beneficiaries can edit the trust, not your parent. Your parent will hold ownership of the assets listed on the trust until their transfer to the beneficiaries.

The significant benefit of an irrevocable trust is that it may not affect your parent’s ability to qualify for Medicaid.

This protects your parent from selling or relinquishing any assets to qualify. If their assets produce any income, they will not be subject to taxation for that income. It can also ensure your parent’s spouse does not lose their home upon passing away.

Testamentary Trusts

A testamentary trust protects your parent if their spouse passes away. When this happens, your parent’s assets are transferred into a testamentary trust, where they will have no control over them.

This type of trust is supposed to protect your parent from fraud and scams and allow them to live without worrying about finances.

Special Needs Trusts

A special needs trust ensures your parent remains eligible for disability benefits while still allowing them to receive income from their assets. Your parent can appoint you or a trusted third party as the trustee where you are responsible for the assets listed.

Special needs trusts are divided into two categories: first-party and third-party trusts. Your parent will be listed as a trust beneficiary. They will receive their own income from any assets, but this income will not affect their eligibility for government benefits.

A third-party trust is where the income is provided by a third party, not from your parent’s assets. The third party can be you and your assets or any other funding source your parents receive.

Step #2: Choosing a Trustee for Your Parent's Trust

Choosing a trustee is one of the most critical decisions when drafting a trust. There are a few factors you must consider before making your decision.

The first factor to consider is the expertise of the trustee.

The trustee will be responsible for all of your parent’s assets. Any errors can mean hefty fines or complications for those involved with the trust. Choosing a family member or individual trustee may cost less, but corporate trustees are safer and ensure compliance and correctness.

The next factor to consider is cost.

To hire a corporate trustee, you will likely pay 1-2% per year for their services. All of the insurance and compliance regulations are included. Compared to hiring a family member or individual trustee, it will likely cost more. However, individuals may hire outside sources, such as accountants or attorneys, to assist in their management.

The other factor is objectivity.

If you choose a family member as the trustee, their decisions may be biased or emotionally charged.

Complex relationships between family members and personal feelings can influence their decision. Corporate trustees are more objective-based but do not have insight into the family.

Related Article: What To Do When A Sibling Is Manipulating Elderly Parent

Step #3: Drafting the Trust Agreement

Drafting a trust agreement may be more straightforward than you think.

The first step is listing all assets your parent wants to include on the trust. This could be property, stocks, bank accounts, physical objects, or anything your parent “owns” and wants to pass on.

The next step is to secure the necessary paperwork associated with the assets to prove ownership. This includes deeds, certificates, titles, and other proof of ownership.

That’s where Trustworthy can help you. We secure and organize important family information, from IDs to money and property information.

After that, you must assign the roles of a trust.

Your parent, alone (not including their spouse), is the sole grantor. Next, your assigned trustee to manage the assets, and finally, the beneficiaries who will receive them.

Once you have the roles assigned and the necessary paperwork, the last step is to fill out the trust document following your state’s laws.

Step #4: Funding the Trust and Transferring Assets

The funding process will differ depending on the type of asset you wish to add to the trust.

However, most physical assets require a simple document to fund all assets in a broad category. For example, all “cash,” “furniture,” or “clothes.”

You require the specific documents outlined in the relevant organization's process to transfer assets like property, business stakes, or finance accounts.

For example, banks typically have designated forms to fill out to transfer a bank account to a trust. The property will require the deed or title of ownership to be transferred.

Contact all parties and companies involved if you have a more specific or complex situation. They will likely tell you directly what is required for them to be able to transfer the asset.

Step #5: Managing and Distributing Trust Assets After Your Parent's Death

After your parent passes away, the trustee will notify the necessary organizations and file the trust with the probate court.

The organizations that need to be notified are the social security administration and the Department of Health. Next, the trustee will notify the beneficiaries of the passing.

The trustee, if responsible, will pay off the grantor’s debts before finally distributing the assets according to the trust’s will. The trustee must legally distribute the assets exactly as the trust dictates.

It is also important to note that depending on the type and amount of the asset a beneficiary receives, they may have to pay taxes for the additional capital.

You should include additional capital, property, or assets when you file your taxes. If not given by a trustee, the beneficiary can legally request exact amounts and values of any assets they receive to aid in filing taxes correctly.

Step #6: Seeking Professional Guidance and Advice

We highly recommend professional guidance to help in the drafting process, distribution of assets, and legal matters. Professional guidance or advice will ensure legal compliance to avoid complications after receiving or distributing assets.

You can request the assistance of trust attorneys, corporate trustees, accountants, or financial advisors. Contact a professional and assemble the relevant documents before drafting your trust. The extra cost will save you effort and ensure a smooth process.

Frequently Asked Questions

What is the best trust for older people?

The best trust for older parents depends on your parent’s specific needs.

A revocable trust will allow them to edit or cancel it anytime. It also protects them from outside forces or beneficiaries from changing the trust. With a revocable trust, your parent can also assign a trusted successor trustee.

On the other hand, an irrevocable trust may not affect your parent’s ability to qualify for Medicaid. It also protects their assets from taxation and ensures the spouse does not lose their home upon passing away.

What type of bank account is best for a trust?

You can set up a trust account at your bank to deposit into or make payments from. The account will not belong to any individual but will be under the trust itself. This ensures the money in the account is subject only to the wishes of the grantor outlined explicitly in the trust.

What assets are best in trust?

The best assets to include in a trust are bank accounts, property, business equity, physical objects, insurance policies, and bonds or stocks. These assets will provide for easy distribution to beneficiaries and avoid excessive taxation.

What is the negative side of trust?

The downsides of a trust are the seemingly complex process and decisions that go into its creation. Giving up control of your assets can be scary, and a trust requires detailed and exact information to be considered legal and valid. There is also the risk of losing tax benefits or being subject to extra taxation with the transfer of assets.

How to Set Up A Trust For An Elderly Parent: 6 Easy Steps

Joel Lim

June 6, 2023

|

The intelligent digital vault for families

Trustworthy protects and optimizes important family information so you can save time, money, and enjoy peace of mind

By setting up a trust for your elderly parent, you can ensure proper, reliable management and handling of your parent’s assets.

So, now you might be wondering how to set up a trust for an elderly parent. That’s exactly what you’ll learn. This article details trusts, their process, and the best way to set one up.

Key Takeaways

Setting up a trust has several benefits, including reduced taxes on procured assets, no probate costs, and protection from scams.

There are several types of trusts to consider, such as revocable, irrevocable, living, testamentary, and special needs trusts. In most cases, an irrevocable trust is the best choice.

Although you can, we would not recommend setting up a trust on your own. Hiring professional guidance to help you with your trust ensures legal compliance and correctness and will save you from any complications in the future.

What is a Trust, and Why Set One Up for an Elderly Parent?

A trust is an arrangement to organize and distribute the assets of a living “grantor.”

A trust involves three parties:

The sole grantor is the legal owner of the assets listed in the trust. In your case, your elderly parent will be the “sole grantor.”

The assets are divided and set to be distributed to the beneficiaries. The beneficiaries can be you, your siblings, family friends, or anybody with a relationship with your parent.

The final role is the trustee. The trustee is responsible for allocating and distributing the assets per the trust after your parent passes away.

There are several benefits to setting up a trust. These benefits include:

Protection from scams, self-management mistakes, and fraud: As your parent gets older, they are more likely to be targets of scam and fraud schemes. They also might lose their ability to manage their finances properly. A trust can protect them by giving control to a more knowledgeable and careful trustee.

Heavily reduced taxes on procured assets: Taxes on assets gained in a trust, like property tax, are much less than those given away during somebody’s lifetime.

No probate costs and no court proceedings: Through a will, the assets and finances of your parent will be distributed through court proceedings. The costs of these proceedings are known as probate costs, which are not applicable or necessary for trusts.

Step #1: Understanding the Different Types of Trusts

Before getting started, it is essential to understand the different types of trusts.

Each type has its specific use and implications.

After you understand each type of trust, you can decide which type will benefit you, your parent, and other beneficiaries the most.

Revocable Trusts

Revocable trusts appoint the grantor as the trustee until they can no longer manage the assets.

This could be through passing away or incapacitation. The grantor designates a successor appointed as the trustee upon the passing or incapacitation.

This type of trust protects your parent by still allowing them a degree of control over their assets. They can edit and adjust the trust as they please. This protects your parent from other beneficiaries or non-trustees from changing the trust in unfavorable ways.

Irrevocable Trusts

Irrevocable trusts involve your parent, the grantor, giving up control to the trustee and other beneficiaries. Unlike revocable trusts, only beneficiaries can edit the trust, not your parent. Your parent will hold ownership of the assets listed on the trust until their transfer to the beneficiaries.

The significant benefit of an irrevocable trust is that it may not affect your parent’s ability to qualify for Medicaid.

This protects your parent from selling or relinquishing any assets to qualify. If their assets produce any income, they will not be subject to taxation for that income. It can also ensure your parent’s spouse does not lose their home upon passing away.

Testamentary Trusts

A testamentary trust protects your parent if their spouse passes away. When this happens, your parent’s assets are transferred into a testamentary trust, where they will have no control over them.

This type of trust is supposed to protect your parent from fraud and scams and allow them to live without worrying about finances.

Special Needs Trusts

A special needs trust ensures your parent remains eligible for disability benefits while still allowing them to receive income from their assets. Your parent can appoint you or a trusted third party as the trustee where you are responsible for the assets listed.

Special needs trusts are divided into two categories: first-party and third-party trusts. Your parent will be listed as a trust beneficiary. They will receive their own income from any assets, but this income will not affect their eligibility for government benefits.

A third-party trust is where the income is provided by a third party, not from your parent’s assets. The third party can be you and your assets or any other funding source your parents receive.

Step #2: Choosing a Trustee for Your Parent's Trust

Choosing a trustee is one of the most critical decisions when drafting a trust. There are a few factors you must consider before making your decision.

The first factor to consider is the expertise of the trustee.

The trustee will be responsible for all of your parent’s assets. Any errors can mean hefty fines or complications for those involved with the trust. Choosing a family member or individual trustee may cost less, but corporate trustees are safer and ensure compliance and correctness.

The next factor to consider is cost.

To hire a corporate trustee, you will likely pay 1-2% per year for their services. All of the insurance and compliance regulations are included. Compared to hiring a family member or individual trustee, it will likely cost more. However, individuals may hire outside sources, such as accountants or attorneys, to assist in their management.

The other factor is objectivity.

If you choose a family member as the trustee, their decisions may be biased or emotionally charged.

Complex relationships between family members and personal feelings can influence their decision. Corporate trustees are more objective-based but do not have insight into the family.

Related Article: What To Do When A Sibling Is Manipulating Elderly Parent

Step #3: Drafting the Trust Agreement

Drafting a trust agreement may be more straightforward than you think.

The first step is listing all assets your parent wants to include on the trust. This could be property, stocks, bank accounts, physical objects, or anything your parent “owns” and wants to pass on.

The next step is to secure the necessary paperwork associated with the assets to prove ownership. This includes deeds, certificates, titles, and other proof of ownership.

That’s where Trustworthy can help you. We secure and organize important family information, from IDs to money and property information.

After that, you must assign the roles of a trust.

Your parent, alone (not including their spouse), is the sole grantor. Next, your assigned trustee to manage the assets, and finally, the beneficiaries who will receive them.

Once you have the roles assigned and the necessary paperwork, the last step is to fill out the trust document following your state’s laws.

Step #4: Funding the Trust and Transferring Assets

The funding process will differ depending on the type of asset you wish to add to the trust.

However, most physical assets require a simple document to fund all assets in a broad category. For example, all “cash,” “furniture,” or “clothes.”

You require the specific documents outlined in the relevant organization's process to transfer assets like property, business stakes, or finance accounts.

For example, banks typically have designated forms to fill out to transfer a bank account to a trust. The property will require the deed or title of ownership to be transferred.

Contact all parties and companies involved if you have a more specific or complex situation. They will likely tell you directly what is required for them to be able to transfer the asset.

Step #5: Managing and Distributing Trust Assets After Your Parent's Death

After your parent passes away, the trustee will notify the necessary organizations and file the trust with the probate court.

The organizations that need to be notified are the social security administration and the Department of Health. Next, the trustee will notify the beneficiaries of the passing.

The trustee, if responsible, will pay off the grantor’s debts before finally distributing the assets according to the trust’s will. The trustee must legally distribute the assets exactly as the trust dictates.

It is also important to note that depending on the type and amount of the asset a beneficiary receives, they may have to pay taxes for the additional capital.

You should include additional capital, property, or assets when you file your taxes. If not given by a trustee, the beneficiary can legally request exact amounts and values of any assets they receive to aid in filing taxes correctly.

Step #6: Seeking Professional Guidance and Advice

We highly recommend professional guidance to help in the drafting process, distribution of assets, and legal matters. Professional guidance or advice will ensure legal compliance to avoid complications after receiving or distributing assets.

You can request the assistance of trust attorneys, corporate trustees, accountants, or financial advisors. Contact a professional and assemble the relevant documents before drafting your trust. The extra cost will save you effort and ensure a smooth process.

Frequently Asked Questions

What is the best trust for older people?

The best trust for older parents depends on your parent’s specific needs.

A revocable trust will allow them to edit or cancel it anytime. It also protects them from outside forces or beneficiaries from changing the trust. With a revocable trust, your parent can also assign a trusted successor trustee.

On the other hand, an irrevocable trust may not affect your parent’s ability to qualify for Medicaid. It also protects their assets from taxation and ensures the spouse does not lose their home upon passing away.

What type of bank account is best for a trust?

You can set up a trust account at your bank to deposit into or make payments from. The account will not belong to any individual but will be under the trust itself. This ensures the money in the account is subject only to the wishes of the grantor outlined explicitly in the trust.

What assets are best in trust?

The best assets to include in a trust are bank accounts, property, business equity, physical objects, insurance policies, and bonds or stocks. These assets will provide for easy distribution to beneficiaries and avoid excessive taxation.

What is the negative side of trust?

The downsides of a trust are the seemingly complex process and decisions that go into its creation. Giving up control of your assets can be scary, and a trust requires detailed and exact information to be considered legal and valid. There is also the risk of losing tax benefits or being subject to extra taxation with the transfer of assets.

How to Set Up A Trust For An Elderly Parent: 6 Easy Steps

Joel Lim

June 6, 2023

|

The intelligent digital vault for families

Trustworthy protects and optimizes important family information so you can save time, money, and enjoy peace of mind

By setting up a trust for your elderly parent, you can ensure proper, reliable management and handling of your parent’s assets.

So, now you might be wondering how to set up a trust for an elderly parent. That’s exactly what you’ll learn. This article details trusts, their process, and the best way to set one up.

Key Takeaways

Setting up a trust has several benefits, including reduced taxes on procured assets, no probate costs, and protection from scams.

There are several types of trusts to consider, such as revocable, irrevocable, living, testamentary, and special needs trusts. In most cases, an irrevocable trust is the best choice.

Although you can, we would not recommend setting up a trust on your own. Hiring professional guidance to help you with your trust ensures legal compliance and correctness and will save you from any complications in the future.

What is a Trust, and Why Set One Up for an Elderly Parent?

A trust is an arrangement to organize and distribute the assets of a living “grantor.”

A trust involves three parties:

The sole grantor is the legal owner of the assets listed in the trust. In your case, your elderly parent will be the “sole grantor.”

The assets are divided and set to be distributed to the beneficiaries. The beneficiaries can be you, your siblings, family friends, or anybody with a relationship with your parent.

The final role is the trustee. The trustee is responsible for allocating and distributing the assets per the trust after your parent passes away.

There are several benefits to setting up a trust. These benefits include:

Protection from scams, self-management mistakes, and fraud: As your parent gets older, they are more likely to be targets of scam and fraud schemes. They also might lose their ability to manage their finances properly. A trust can protect them by giving control to a more knowledgeable and careful trustee.

Heavily reduced taxes on procured assets: Taxes on assets gained in a trust, like property tax, are much less than those given away during somebody’s lifetime.

No probate costs and no court proceedings: Through a will, the assets and finances of your parent will be distributed through court proceedings. The costs of these proceedings are known as probate costs, which are not applicable or necessary for trusts.

Step #1: Understanding the Different Types of Trusts

Before getting started, it is essential to understand the different types of trusts.

Each type has its specific use and implications.

After you understand each type of trust, you can decide which type will benefit you, your parent, and other beneficiaries the most.

Revocable Trusts

Revocable trusts appoint the grantor as the trustee until they can no longer manage the assets.

This could be through passing away or incapacitation. The grantor designates a successor appointed as the trustee upon the passing or incapacitation.

This type of trust protects your parent by still allowing them a degree of control over their assets. They can edit and adjust the trust as they please. This protects your parent from other beneficiaries or non-trustees from changing the trust in unfavorable ways.

Irrevocable Trusts

Irrevocable trusts involve your parent, the grantor, giving up control to the trustee and other beneficiaries. Unlike revocable trusts, only beneficiaries can edit the trust, not your parent. Your parent will hold ownership of the assets listed on the trust until their transfer to the beneficiaries.

The significant benefit of an irrevocable trust is that it may not affect your parent’s ability to qualify for Medicaid.

This protects your parent from selling or relinquishing any assets to qualify. If their assets produce any income, they will not be subject to taxation for that income. It can also ensure your parent’s spouse does not lose their home upon passing away.

Testamentary Trusts

A testamentary trust protects your parent if their spouse passes away. When this happens, your parent’s assets are transferred into a testamentary trust, where they will have no control over them.

This type of trust is supposed to protect your parent from fraud and scams and allow them to live without worrying about finances.

Special Needs Trusts

A special needs trust ensures your parent remains eligible for disability benefits while still allowing them to receive income from their assets. Your parent can appoint you or a trusted third party as the trustee where you are responsible for the assets listed.

Special needs trusts are divided into two categories: first-party and third-party trusts. Your parent will be listed as a trust beneficiary. They will receive their own income from any assets, but this income will not affect their eligibility for government benefits.

A third-party trust is where the income is provided by a third party, not from your parent’s assets. The third party can be you and your assets or any other funding source your parents receive.

Step #2: Choosing a Trustee for Your Parent's Trust

Choosing a trustee is one of the most critical decisions when drafting a trust. There are a few factors you must consider before making your decision.

The first factor to consider is the expertise of the trustee.

The trustee will be responsible for all of your parent’s assets. Any errors can mean hefty fines or complications for those involved with the trust. Choosing a family member or individual trustee may cost less, but corporate trustees are safer and ensure compliance and correctness.

The next factor to consider is cost.

To hire a corporate trustee, you will likely pay 1-2% per year for their services. All of the insurance and compliance regulations are included. Compared to hiring a family member or individual trustee, it will likely cost more. However, individuals may hire outside sources, such as accountants or attorneys, to assist in their management.

The other factor is objectivity.

If you choose a family member as the trustee, their decisions may be biased or emotionally charged.

Complex relationships between family members and personal feelings can influence their decision. Corporate trustees are more objective-based but do not have insight into the family.

Related Article: What To Do When A Sibling Is Manipulating Elderly Parent

Step #3: Drafting the Trust Agreement

Drafting a trust agreement may be more straightforward than you think.

The first step is listing all assets your parent wants to include on the trust. This could be property, stocks, bank accounts, physical objects, or anything your parent “owns” and wants to pass on.

The next step is to secure the necessary paperwork associated with the assets to prove ownership. This includes deeds, certificates, titles, and other proof of ownership.

That’s where Trustworthy can help you. We secure and organize important family information, from IDs to money and property information.

After that, you must assign the roles of a trust.

Your parent, alone (not including their spouse), is the sole grantor. Next, your assigned trustee to manage the assets, and finally, the beneficiaries who will receive them.

Once you have the roles assigned and the necessary paperwork, the last step is to fill out the trust document following your state’s laws.

Step #4: Funding the Trust and Transferring Assets

The funding process will differ depending on the type of asset you wish to add to the trust.

However, most physical assets require a simple document to fund all assets in a broad category. For example, all “cash,” “furniture,” or “clothes.”

You require the specific documents outlined in the relevant organization's process to transfer assets like property, business stakes, or finance accounts.

For example, banks typically have designated forms to fill out to transfer a bank account to a trust. The property will require the deed or title of ownership to be transferred.

Contact all parties and companies involved if you have a more specific or complex situation. They will likely tell you directly what is required for them to be able to transfer the asset.

Step #5: Managing and Distributing Trust Assets After Your Parent's Death

After your parent passes away, the trustee will notify the necessary organizations and file the trust with the probate court.

The organizations that need to be notified are the social security administration and the Department of Health. Next, the trustee will notify the beneficiaries of the passing.

The trustee, if responsible, will pay off the grantor’s debts before finally distributing the assets according to the trust’s will. The trustee must legally distribute the assets exactly as the trust dictates.

It is also important to note that depending on the type and amount of the asset a beneficiary receives, they may have to pay taxes for the additional capital.

You should include additional capital, property, or assets when you file your taxes. If not given by a trustee, the beneficiary can legally request exact amounts and values of any assets they receive to aid in filing taxes correctly.

Step #6: Seeking Professional Guidance and Advice

We highly recommend professional guidance to help in the drafting process, distribution of assets, and legal matters. Professional guidance or advice will ensure legal compliance to avoid complications after receiving or distributing assets.

You can request the assistance of trust attorneys, corporate trustees, accountants, or financial advisors. Contact a professional and assemble the relevant documents before drafting your trust. The extra cost will save you effort and ensure a smooth process.

Frequently Asked Questions

What is the best trust for older people?

The best trust for older parents depends on your parent’s specific needs.

A revocable trust will allow them to edit or cancel it anytime. It also protects them from outside forces or beneficiaries from changing the trust. With a revocable trust, your parent can also assign a trusted successor trustee.

On the other hand, an irrevocable trust may not affect your parent’s ability to qualify for Medicaid. It also protects their assets from taxation and ensures the spouse does not lose their home upon passing away.

What type of bank account is best for a trust?

You can set up a trust account at your bank to deposit into or make payments from. The account will not belong to any individual but will be under the trust itself. This ensures the money in the account is subject only to the wishes of the grantor outlined explicitly in the trust.

What assets are best in trust?

The best assets to include in a trust are bank accounts, property, business equity, physical objects, insurance policies, and bonds or stocks. These assets will provide for easy distribution to beneficiaries and avoid excessive taxation.

What is the negative side of trust?

The downsides of a trust are the seemingly complex process and decisions that go into its creation. Giving up control of your assets can be scary, and a trust requires detailed and exact information to be considered legal and valid. There is also the risk of losing tax benefits or being subject to extra taxation with the transfer of assets.

Try Trustworthy today.

Try Trustworthy today.

Try the Family Operating System® for yourself. You (and your family) will love it.

Try the Family Operating System® for yourself. You (and your family) will love it.

No credit card required.

No credit card required.

Related Articles

May 15, 2024

May 15, 2024

Power of Attorney vs. Will: Understanding the Legal Authority

Power of Attorney vs. Will: Understanding the Legal Authority

May 15, 2024

May 15, 2024

Executor Fees: What Percentage of an Estate Is Typical?

Executor Fees: What Percentage of an Estate Is Typical?

May 9, 2024

May 9, 2024

Power of Attorney Liability: Risks and Responsibilities

Power of Attorney Liability: Risks and Responsibilities

May 9, 2024

May 9, 2024

The Timeline for Obtaining Power of Attorney Explained

The Timeline for Obtaining Power of Attorney Explained

May 7, 2024

May 7, 2024

The Comprehensive Guide to Power of Attorney Responsibilities

The Comprehensive Guide to Power of Attorney Responsibilities

May 3, 2024

May 3, 2024

Deceased's Property: How Long Before It Must Change Names?

Deceased's Property: How Long Before It Must Change Names?

Apr 26, 2024

Apr 26, 2024

Durable Power of Attorney: What Powers Does It Grant?

Durable Power of Attorney: What Powers Does It Grant?

Apr 26, 2024

Apr 26, 2024

How to Draft a Power of Attorney: A Step-by-Step Guide

How to Draft a Power of Attorney: A Step-by-Step Guide

Apr 23, 2024

Apr 23, 2024

Executor's Death: The Next Steps for an Estate

Executor's Death: The Next Steps for an Estate

Apr 19, 2024

Apr 19, 2024

Removing a Deceased Spouse from a Deed: 5 Necessary Steps

Removing a Deceased Spouse from a Deed: 5 Necessary Steps

Apr 17, 2024

Apr 17, 2024

After Death: Can a Spouse Change the Deceased's Will?

After Death: Can a Spouse Change the Deceased's Will?

Apr 17, 2024

Apr 17, 2024

Divorced Spouse's Rights to Property After Death Explained

Divorced Spouse's Rights to Property After Death Explained

Apr 11, 2024

Apr 11, 2024

Navigating Dual Benefits: VA Disability and Social Security

Navigating Dual Benefits: VA Disability and Social Security

Apr 11, 2024

Apr 11, 2024

Veteran Benefit Eligibility: Understanding Denials and Exclusions

Veteran Benefit Eligibility: Understanding Denials and Exclusions

Apr 4, 2024

Apr 4, 2024

Eligibility for Veteran’s Spouse Benefits: What You Need to Know

Eligibility for Veteran’s Spouse Benefits: What You Need to Know

Apr 3, 2024

Apr 3, 2024

VA Disability Payments: Can They Be Discontinued?

VA Disability Payments: Can They Be Discontinued?

Mar 30, 2024

Mar 30, 2024

Veteran Death: Essential Actions and Checklist for Next of Kin

Veteran Death: Essential Actions and Checklist for Next of Kin

Mar 27, 2024

Mar 27, 2024

SLATs in Estate Planning: An Innovative Strategy Explained

SLATs in Estate Planning: An Innovative Strategy Explained

Mar 27, 2024

Mar 27, 2024

Maximize Your Estate Planning with Survivorship Life Insurance

Maximize Your Estate Planning with Survivorship Life Insurance

Mar 23, 2024

Mar 23, 2024

VA Benefits Timeline: When They Stop After Death

VA Benefits Timeline: When They Stop After Death

Mar 20, 2024

Mar 20, 2024

Is Estate Planning a Legitimate Business Expense: Unveiling The Truth

Is Estate Planning a Legitimate Business Expense: Unveiling The Truth

Mar 15, 2024

Mar 15, 2024

Does Right of Survivorship Trump a Will: Legal Insights

Does Right of Survivorship Trump a Will: Legal Insights

Mar 13, 2024

Mar 13, 2024

Palliative Care at Home: Understanding Insurance Coverage

Palliative Care at Home: Understanding Insurance Coverage

Mar 13, 2024

Mar 13, 2024

Navigating Insurance Coverage for Hospice Care A Complete Guide

Navigating Insurance Coverage for Hospice Care A Complete Guide

Mar 9, 2024

Mar 9, 2024

Choosing an Estate Planning Attorney: Traits of Excellence

Choosing an Estate Planning Attorney: Traits of Excellence

Mar 7, 2024

Mar 7, 2024

Can Family Overrule an Advance Directive? What You Need to Know

Can Family Overrule an Advance Directive? What You Need to Know

Mar 7, 2024

Mar 7, 2024

Funding Hospice Care in Nursing Homes: Who Bears the Cost?

Funding Hospice Care in Nursing Homes: Who Bears the Cost?

Mar 5, 2024

Mar 5, 2024

Who Can Legally Witness an Advance Directive? Know Your Rights

Who Can Legally Witness an Advance Directive? Know Your Rights

Mar 5, 2024

Mar 5, 2024

Exploring Hospice Care: What’s Not Included?

Exploring Hospice Care: What’s Not Included?

Mar 5, 2024

Mar 5, 2024

Respite Care in Hospice: Providing Relief for Caregivers

Respite Care in Hospice: Providing Relief for Caregivers

Mar 5, 2024

Mar 5, 2024

Exploring the Spectrum: Different Types of Advance Directives

Exploring the Spectrum: Different Types of Advance Directives

Feb 28, 2024

Feb 28, 2024

Deciding on Hospice Care: Knowing When It's Time

Deciding on Hospice Care: Knowing When It's Time

Feb 27, 2024

Feb 27, 2024

Hospice Care Duration: How Long Can It Last?

Hospice Care Duration: How Long Can It Last?

Feb 27, 2024

Feb 27, 2024

Hospice Care Timeline: Estimating How Long to Live

Hospice Care Timeline: Estimating How Long to Live

Feb 22, 2024

Feb 22, 2024

Doctor-Ordered Hospice Care: When and Why It Happens

Doctor-Ordered Hospice Care: When and Why It Happens

Feb 20, 2024

Feb 20, 2024

Funeral Planning Timeline: How Long Does it Really Take?

Funeral Planning Timeline: How Long Does it Really Take?

Feb 15, 2024

Feb 15, 2024

Writing a Heartfelt Obituary for Your Husband: Inspiring Examples

Writing a Heartfelt Obituary for Your Husband: Inspiring Examples

Feb 14, 2024

Feb 14, 2024

Planning Your Funeral: The Best Age To Start

Planning Your Funeral: The Best Age To Start

Feb 14, 2024

Feb 14, 2024

Crafting a Loving Obituary For Your Son: Meaningful Examples

Crafting a Loving Obituary For Your Son: Meaningful Examples

Jan 18, 2024

Jan 18, 2024

Improving Communication Between Caregivers and Doctors

Improving Communication Between Caregivers and Doctors

Nov 29, 2023

Nov 29, 2023

Can Anyone Get a Copy of a Death Certificate? Who Is Authorized?

Can Anyone Get a Copy of a Death Certificate? Who Is Authorized?

Nov 25, 2023

Nov 25, 2023

Original Death Certificate vs. Certified Copy: Key Differences And Why They Matter

Original Death Certificate vs. Certified Copy: Key Differences And Why They Matter

Nov 25, 2023

Nov 25, 2023

How Do You Handle Negative Aspects of the Deceased's Life in a Eulogy?

How Do You Handle Negative Aspects of the Deceased's Life in a Eulogy?

Nov 25, 2023

Nov 25, 2023

Can There Be More Then One Eulogy at a Funeral? Etiquette Explained

Can There Be More Then One Eulogy at a Funeral? Etiquette Explained

Nov 24, 2023

Nov 24, 2023

My Dad Died, Can I Get His Retirement Pension?

My Dad Died, Can I Get His Retirement Pension?

Nov 24, 2023

Nov 24, 2023

How Many Copies of a Death Certificate Should You Get?

How Many Copies of a Death Certificate Should You Get?

Nov 24, 2023

Nov 24, 2023

Can a Eulogy Be Funny? Yes, Here Are 10 Respectful but Funny Examples

Can a Eulogy Be Funny? Yes, Here Are 10 Respectful but Funny Examples

Nov 24, 2023

Nov 24, 2023

How Do You Receive Inheritance Money WITHOUT any issues?

How Do You Receive Inheritance Money WITHOUT any issues?

Nov 17, 2023

Nov 17, 2023

Who Gets The Tax Refund of A Deceased Person? An Accountant Answers

Who Gets The Tax Refund of A Deceased Person? An Accountant Answers

Nov 17, 2023

Nov 17, 2023

How To Start a Eulogy: 15 Heartfelt Examples

How To Start a Eulogy: 15 Heartfelt Examples

Nov 14, 2023

Nov 14, 2023

How To Discuss End-of-Life Care With Parents (Simple Guide)

How To Discuss End-of-Life Care With Parents (Simple Guide)

Nov 14, 2023

Nov 14, 2023

How To Cancel a Deceased Person's Subscriptions the EASY Way

How To Cancel a Deceased Person's Subscriptions the EASY Way

Nov 8, 2023

Nov 8, 2023

What Should You Not Put in a Eulogy (9 Things To Avoid)

What Should You Not Put in a Eulogy (9 Things To Avoid)

Nov 7, 2023

Nov 7, 2023

How Are Estates Distributed If There's No Will? A Lawyer Explains Intestate

How Are Estates Distributed If There's No Will? A Lawyer Explains Intestate

Nov 6, 2023

Nov 6, 2023

Does Microsoft Word Have an Obituary Template?

Does Microsoft Word Have an Obituary Template?

Nov 6, 2023

Nov 6, 2023

How To Post an Obituary on Facebook: A Step-by-Step Guide

How To Post an Obituary on Facebook: A Step-by-Step Guide

Nov 6, 2023

Nov 6, 2023

Why Do You Need A Death Certificate For Estate & Probate Process?

Why Do You Need A Death Certificate For Estate & Probate Process?

Nov 2, 2023

Nov 2, 2023

How Do I Correct Errors on a Death Certificate? And, How Long Does It Take?

How Do I Correct Errors on a Death Certificate? And, How Long Does It Take?

Nov 2, 2023

Nov 2, 2023

12 Steps For Writing a Eulogy For Mom

12 Steps For Writing a Eulogy For Mom

Nov 2, 2023

Nov 2, 2023

12 Steps for Writing a Eulogy for Dad

12 Steps for Writing a Eulogy for Dad

Nov 1, 2023

Nov 1, 2023

Who Does The Obituary When Someone Dies?

Who Does The Obituary When Someone Dies?

Nov 1, 2023

Nov 1, 2023

How Late Is Too Late For An Obituary? 6 Steps To Take Today

How Late Is Too Late For An Obituary? 6 Steps To Take Today

Nov 1, 2023

Nov 1, 2023

How Much Does It Cost To Publish An Obituary? Breaking It Down

How Much Does It Cost To Publish An Obituary? Breaking It Down

Nov 1, 2023

Nov 1, 2023

6 Reasons You Need an Obituary (Plus 6 Reasons You Don't)

6 Reasons You Need an Obituary (Plus 6 Reasons You Don't)

Oct 30, 2023

Oct 30, 2023

Where Do You Post an Obituary: A Step-By-Step Guide

Where Do You Post an Obituary: A Step-By-Step Guide

Oct 30, 2023

Oct 30, 2023

Obituary vs Death Note: What Are the Key Differences?

Obituary vs Death Note: What Are the Key Differences?

Oct 5, 2023

Oct 5, 2023

Buying A House With Elderly Parent: 10 Things To Know

Buying A House With Elderly Parent: 10 Things To Know

Sep 14, 2023

Sep 14, 2023

I'm Trapped Caring for Elderly Parents

I'm Trapped Caring for Elderly Parents

Oct 5, 2023

Oct 5, 2023

401(k) and Minors: Can a Minor be a Beneficiary?

401(k) and Minors: Can a Minor be a Beneficiary?

Sep 12, 2023

Sep 12, 2023

How to Self-Direct Your 401(k): Take Control of Your Retirement

How to Self-Direct Your 401(k): Take Control of Your Retirement

Aug 3, 2023

Aug 3, 2023

The Ultimate Guide to Decluttering and Simplifying Your Home as You Age

The Ultimate Guide to Decluttering and Simplifying Your Home as You Age

Aug 3, 2023

Aug 3, 2023

The Essential Guide to Preparing for Retirement

The Essential Guide to Preparing for Retirement

Aug 3, 2023

Aug 3, 2023

Estate Planning For Blended Families (Complete Guide)

Estate Planning For Blended Families (Complete Guide)

Aug 3, 2023

Aug 3, 2023

Estate Planning For Physicians (Complete Guide)

Estate Planning For Physicians (Complete Guide)

Jul 14, 2023

Jul 14, 2023

Are You Legally Responsible For Your Elderly Parents?

Are You Legally Responsible For Your Elderly Parents?

Jun 7, 2023

Jun 7, 2023

How To Travel With Elderly Parent: Here's How to Prepare

How To Travel With Elderly Parent: Here's How to Prepare

Jun 6, 2023

Jun 6, 2023

Checklist For Moving A Parent To Assisted Living

Checklist For Moving A Parent To Assisted Living

Jun 6, 2023

Jun 6, 2023

How to Set Up A Trust For An Elderly Parent: 6 Easy Steps

How to Set Up A Trust For An Elderly Parent: 6 Easy Steps

Jun 6, 2023

Jun 6, 2023

How To Stop Elderly Parents From Giving Money Away (9 Tips)

How To Stop Elderly Parents From Giving Money Away (9 Tips)

Jun 6, 2023

Jun 6, 2023

Should Elderly Parents Sign Over Their House? Pros & Cons

Should Elderly Parents Sign Over Their House? Pros & Cons

May 17, 2023

May 17, 2023

Estate Planning: A Comprehensive Guide

Estate Planning: A Comprehensive Guide

May 2, 2023

May 2, 2023

Helping Elderly Parents: The Complete Guide

Helping Elderly Parents: The Complete Guide

May 1, 2023

May 1, 2023

Trustworthy guide: How to organize your digital information

Trustworthy guide: How to organize your digital information

Apr 15, 2023

Apr 15, 2023

Can My Husband Make a Will Without My Knowledge?

Can My Husband Make a Will Without My Knowledge?

Apr 15, 2023

Apr 15, 2023

What is a Last Will and Testament (also known as a Will)?

What is a Last Will and Testament (also known as a Will)?

Apr 15, 2023

Apr 15, 2023

Can A Wife Sell Deceased Husband's Property (6 Rules)

Can A Wife Sell Deceased Husband's Property (6 Rules)

Apr 15, 2023

Apr 15, 2023

Should I Shred Documents Of A Deceased Person? (5 Tips)

Should I Shred Documents Of A Deceased Person? (5 Tips)

Apr 15, 2023

Apr 15, 2023

Can I Change My Power of Attorney Without A Lawyer?

Can I Change My Power of Attorney Without A Lawyer?

Apr 15, 2023

Apr 15, 2023

Can You Have Two Power of Attorneys? (A Lawyer Answers)

Can You Have Two Power of Attorneys? (A Lawyer Answers)

Apr 15, 2023

Apr 15, 2023

Do Attorneys Keep Copies Of a Will? (4 Things To Know)

Do Attorneys Keep Copies Of a Will? (4 Things To Know)

Apr 15, 2023

Apr 15, 2023

Estate Planning for a Special Needs Child (Complete Guide)

Estate Planning for a Special Needs Child (Complete Guide)

Apr 15, 2023

Apr 15, 2023

Estate Planning For Childless Couples (Complete Guide)

Estate Planning For Childless Couples (Complete Guide)

Apr 15, 2023

Apr 15, 2023

Estate Planning For Elderly Parents (Complete Guide)

Estate Planning For Elderly Parents (Complete Guide)

Apr 15, 2023

Apr 15, 2023

Estate Planning For High Net Worth & Large Estates

Estate Planning For High Net Worth & Large Estates

Apr 15, 2023

Apr 15, 2023

Estate Planning For Irresponsible Children (Complete Guide)

Estate Planning For Irresponsible Children (Complete Guide)

Apr 15, 2023

Apr 15, 2023

How To Get Power of Attorney For Parent With Dementia?

How To Get Power of Attorney For Parent With Dementia?

Apr 15, 2023

Apr 15, 2023

I Lost My Power of Attorney Papers, Now What?

I Lost My Power of Attorney Papers, Now What?

Apr 15, 2023

Apr 15, 2023

Is It Better To Sell or Rent An Inherited House? (Pros & Cons)

Is It Better To Sell or Rent An Inherited House? (Pros & Cons)

Apr 15, 2023

Apr 15, 2023

Is It Wrong To Move Away From Elderly Parents? My Advice

Is It Wrong To Move Away From Elderly Parents? My Advice

Apr 15, 2023

Apr 15, 2023

Moving An Elderly Parent Into Your Home: What To Know

Moving An Elderly Parent Into Your Home: What To Know

Apr 15, 2023

Apr 15, 2023

Moving An Elderly Parent to Another State: What To Know

Moving An Elderly Parent to Another State: What To Know

Apr 15, 2023

Apr 15, 2023

What If Witnesses To A Will Cannot Be Found? A Lawyer Answers

What If Witnesses To A Will Cannot Be Found? A Lawyer Answers

Apr 15, 2023

Apr 15, 2023

What To Bring To Estate Planning Meeting (Checklist)

What To Bring To Estate Planning Meeting (Checklist)

Apr 15, 2023

Apr 15, 2023

When Should You Get An Estate Plan? (According To A Lawyer)

When Should You Get An Estate Plan? (According To A Lawyer)

Apr 15, 2023

Apr 15, 2023

Which Sibling Should Take Care of Elderly Parents?

Which Sibling Should Take Care of Elderly Parents?

Apr 15, 2023

Apr 15, 2023

Who Can Override A Power of Attorney? (A Lawyer Answers)

Who Can Override A Power of Attorney? (A Lawyer Answers)

Apr 15, 2023

Apr 15, 2023

Can Power of Attorney Sell Property Before Death?

Can Power of Attorney Sell Property Before Death?

Apr 15, 2023

Apr 15, 2023

Can The Executor Of A Will Access Bank Accounts? (Yes, Here's How)

Can The Executor Of A Will Access Bank Accounts? (Yes, Here's How)

Apr 15, 2023

Apr 15, 2023

Complete List of Things To Do For Elderly Parents (Checklist)

Complete List of Things To Do For Elderly Parents (Checklist)

Apr 15, 2023

Apr 15, 2023

How To Get Power of Attorney For A Deceased Person?

How To Get Power of Attorney For A Deceased Person?

Apr 15, 2023

Apr 15, 2023

How To Help Elderly Parents From A Distance? 7 Tips

How To Help Elderly Parents From A Distance? 7 Tips

Apr 15, 2023

Apr 15, 2023

Legal Documents For Elderly Parents: Checklist

Legal Documents For Elderly Parents: Checklist

Apr 15, 2023

Apr 15, 2023

Selling Elderly Parents Home: How To Do It + Mistakes To Avoid

Selling Elderly Parents Home: How To Do It + Mistakes To Avoid

Apr 15, 2023

Apr 15, 2023

What To Do When A Sibling Is Manipulating Elderly Parents

What To Do When A Sibling Is Manipulating Elderly Parents

Apr 6, 2023

Apr 6, 2023

Can An Out of State Attorney Write My Will? (A Lawyer Answers)

Can An Out of State Attorney Write My Will? (A Lawyer Answers)

Mar 15, 2023

Mar 15, 2023

Settling an Estate: A Step-by-Step Guide

Settling an Estate: A Step-by-Step Guide

Feb 10, 2023

Feb 10, 2023

My Deceased Husband Received A Check In The Mail (4 Steps To Take)

My Deceased Husband Received A Check In The Mail (4 Steps To Take)

Feb 7, 2023

Feb 7, 2023

The Benefits of Working With an Experienced Estate Planning Attorney

The Benefits of Working With an Experienced Estate Planning Attorney

Feb 6, 2023

Feb 6, 2023

How To Track Elderly Parents' Phone (2 Options)

How To Track Elderly Parents' Phone (2 Options)

Feb 1, 2023

Feb 1, 2023

Can You Collect Your Parents' Social Security When They Die?

Can You Collect Your Parents' Social Security When They Die?

Feb 1, 2023

Feb 1, 2023

How Do I Stop VA Benefits When Someone Dies (Simple Guide)

How Do I Stop VA Benefits When Someone Dies (Simple Guide)

Feb 1, 2023

Feb 1, 2023

Can You Pay Money Into A Deceased Person's Bank Account?

Can You Pay Money Into A Deceased Person's Bank Account?

Feb 1, 2023

Feb 1, 2023

Deleting A Facebook Account When Someone Dies (Step by Step)

Deleting A Facebook Account When Someone Dies (Step by Step)

Feb 1, 2023

Feb 1, 2023

Does The DMV Know When Someone Dies?

Does The DMV Know When Someone Dies?

Feb 1, 2023

Feb 1, 2023

How To Find A Deceased Person's Lawyer (5 Ways)

How To Find A Deceased Person's Lawyer (5 Ways)

Feb 1, 2023

Feb 1, 2023

How To Plan A Celebration Of Life (10 Steps With Examples)

How To Plan A Celebration Of Life (10 Steps With Examples)

Feb 1, 2023

Feb 1, 2023

How To Stop Mail Of A Deceased Person? A Simple Guide

How To Stop Mail Of A Deceased Person? A Simple Guide

Feb 1, 2023

Feb 1, 2023

How to Stop Social Security Direct Deposit After Death

How to Stop Social Security Direct Deposit After Death

Feb 1, 2023

Feb 1, 2023

How To Transfer Firearms From A Deceased Person (3 Steps)

How To Transfer Firearms From A Deceased Person (3 Steps)

Feb 1, 2023

Feb 1, 2023

How To Write An Obituary (5 Steps With Examples)

How To Write An Obituary (5 Steps With Examples)

Feb 1, 2023

Feb 1, 2023

What Happens To A Leased Vehicle When Someone Dies?

What Happens To A Leased Vehicle When Someone Dies?

Jan 31, 2023

Jan 31, 2023

Do Wills Expire? 6 Things To Know

Do Wills Expire? 6 Things To Know

Jan 31, 2023

Jan 31, 2023

How To Get Into a Deceased Person's Computer (Microsoft & Apple)

How To Get Into a Deceased Person's Computer (Microsoft & Apple)

Jan 31, 2023

Jan 31, 2023

Why Do Funeral Homes Take Fingerprints of the Deceased?

Why Do Funeral Homes Take Fingerprints of the Deceased?

Jan 31, 2023

Jan 31, 2023

What To Do If Your Deceased Parents' Home Is In Foreclosure

What To Do If Your Deceased Parents' Home Is In Foreclosure

Jan 31, 2023

Jan 31, 2023

Questions To Ask An Estate Attorney After Death (Checklist)

Questions To Ask An Estate Attorney After Death (Checklist)

Jan 31, 2023

Jan 31, 2023

What Happens If a Deceased Individual Owes Taxes?

What Happens If a Deceased Individual Owes Taxes?

Jan 31, 2023

Jan 31, 2023

Components of Estate Planning: 6 Things To Consider

Components of Estate Planning: 6 Things To Consider

Jan 22, 2023

Jan 22, 2023

What To Do If Insurance Check Is Made Out To A Deceased Person

What To Do If Insurance Check Is Made Out To A Deceased Person

Jan 8, 2023

Jan 8, 2023

What Does a Typical Estate Plan Include?

What Does a Typical Estate Plan Include?

Apr 15, 2022

Apr 15, 2022

Can I Do A Video Will? (Is It Legitimate & What To Consider)

Can I Do A Video Will? (Is It Legitimate & What To Consider)

Apr 15, 2022

Apr 15, 2022

Estate Planning For Green Card Holders (Complete Guide)

Estate Planning For Green Card Holders (Complete Guide)

Mar 2, 2022

Mar 2, 2022

What Does Your “Property” Mean?

What Does Your “Property” Mean?

Mar 2, 2022

Mar 2, 2022

What is the Uniform Trust Code? What is the Uniform Probate Code?

What is the Uniform Trust Code? What is the Uniform Probate Code?

Mar 2, 2022

Mar 2, 2022

Do You Need to Avoid Probate?

Do You Need to Avoid Probate?

Mar 2, 2022

Mar 2, 2022

How is a Trust Created?

How is a Trust Created?

Mar 2, 2022

Mar 2, 2022

What Are Advance Directives?

What Are Advance Directives?

Mar 2, 2022

Mar 2, 2022

What does a Trustee Do?

What does a Trustee Do?

Mar 2, 2022

Mar 2, 2022

What is an Estate Plan? (And why you need one)

What is an Estate Plan? (And why you need one)

Mar 2, 2022

Mar 2, 2022

What is Probate?

What is Probate?

Mar 2, 2022

Mar 2, 2022

What Is Your Domicile & Why It Matters

What Is Your Domicile & Why It Matters

Mar 2, 2022

Mar 2, 2022

What Is a Power of Attorney for Finances?

What Is a Power of Attorney for Finances?

Mar 1, 2022

Mar 1, 2022

Should your family consider an umbrella insurance policy?

Should your family consider an umbrella insurance policy?

Mar 1, 2022

Mar 1, 2022

Do I need a digital power of attorney?

Do I need a digital power of attorney?

Apr 6, 2020

Apr 6, 2020

What Exactly is a Trust?

What Exactly is a Trust?